If you're an FMCG brand expanding into general trade — especially into a new state — you need to understand one thing before anything else: the margin stack is the single most important factor in whether your product gets pushed, gets stocked, or gets ignored. Not your packaging. Not your advertising. The margin. This article breaks down the full margin structure in GT, from MRP to retailer to distributor, and explains how to price your product for a new market. For the broader context of how GT distribution works, see our Complete Guide to FMCG Distribution in India.

The Full Margin Stack

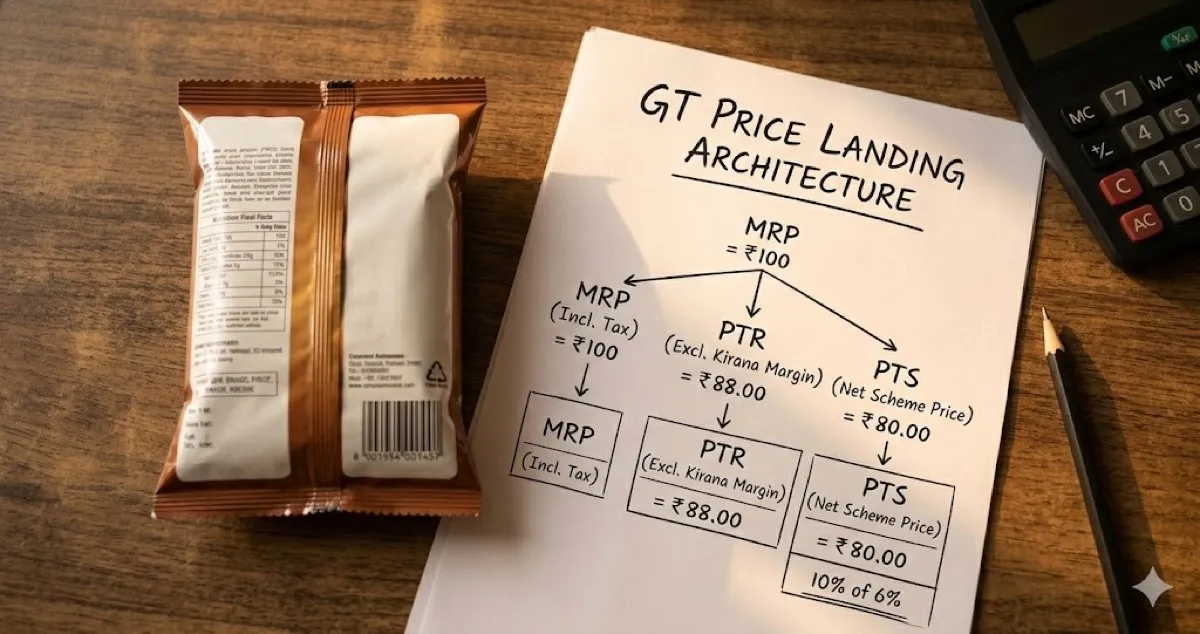

In general trade, the price flows downward from MRP through several layers, each taking a cut:

MRP → Retailer Purchase Price (PTR) → Distributor Purchase Price (PTS) → Brand Net Realization

Here is a simplified example for a product with an MRP of ₹100:

| Layer | Price | Margin |

|---|---|---|

| MRP (Consumer pays) | ₹100 | — |

| Retailer buys at (PTR) | ₹85 | ~15% on MRP |

| Distributor buys at (PTS) | ₹76 | ~10% on PTR |

| Brand net realization | ₹70–74 | After schemes, freight, damages |

| Super Stockist (if applicable) | ₹73–75 | 2–3% handling/buffer margin |

The exact numbers vary by category, brand strength, and geography. But the structure is consistent. For a detailed walkthrough of how to set MRP, PTR, and PTS, read GT Pricing Architecture: MRP, PTR, PTS Explained.

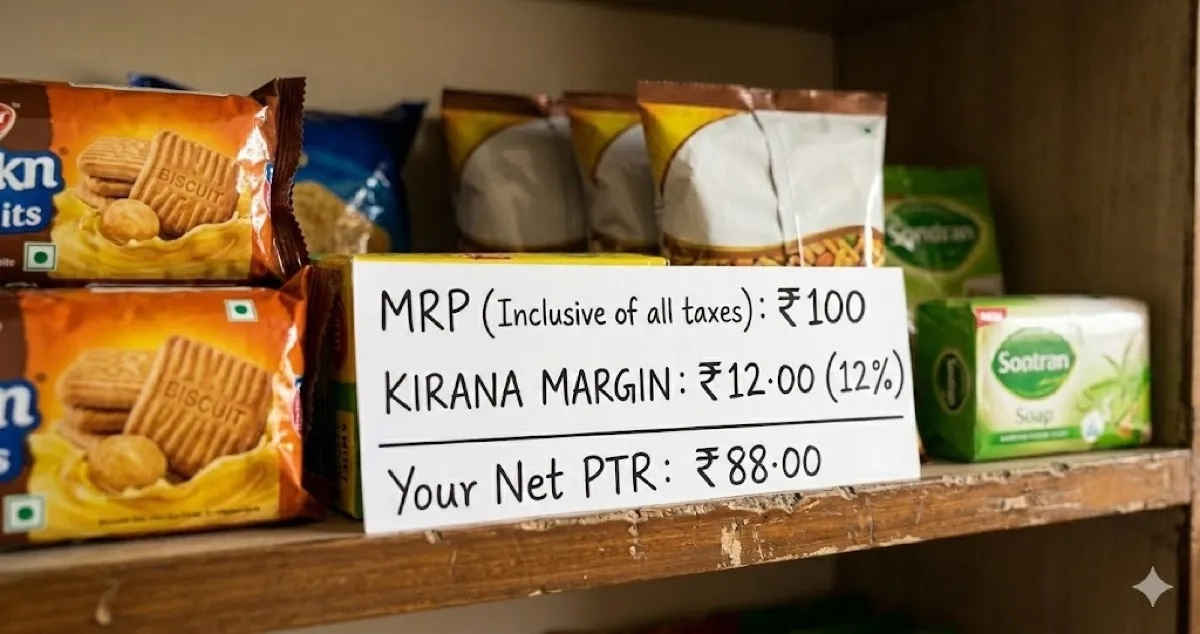

Why Retailer Margin Is the Most Important Number

The kirana retailer is the gatekeeper. If the retailer doesn't stock your product — or stocks it but doesn't recommend it — you have no sales. Retailer margin expectations depend on three things:

National brands with strong consumer pull (Parle, Britannia, HUL): Retailers accept 5–10% margin because the product sells itself. Consumers walk in and ask for it by name. The retailer doesn't need to push it.

Regional brands with moderate recognition: Retailers expect 10–18%. The product has some pull in certain pockets, but the retailer needs a reason to allocate shelf space and occasionally recommend it over alternatives.

New or unknown brands entering a new state: Retailers demand 18–25% or more. They're taking a risk — tying up shelf space and capital for a product that may not move. Higher margin compensates for that risk. If the product doesn't rotate in 2–3 weeks, the retailer will push it to the back or stop reordering entirely.

Understanding how kirana stores decide what to stock is essential to getting this right.

The Hidden Costs That Don't Show Up on the Term Sheet

Most brands calculate distribution cost as “distributor margin + retailer margin.” But the real cost is significantly higher. Here are the five hidden costs that erode your net realization:

- Credit losses: In GT, the distributor extends credit to retailers (typically 7–15 days). Some of that credit goes bad. If your distributor has a 2–3% credit loss rate, that cost gets passed back to you — either directly or through higher margin demands. The more you expand into unfamiliar markets, the higher this risk. Read more in Credit Risk and Collections in GT.

- Returns and expiry: Products that don't rotate fast enough expire on shelves. The retailer returns them to the distributor, who claims them from you. For a new brand in a new market, a 3–5% return rate in the first year is common. In some categories (dairy, bakery), it's much higher.

- Scheme funding: Trade schemes (buy X get Y, introductory discounts, display incentives) are essential to drive initial trial. But they add 5–15% to your effective cost of sales. Brands often budget for the initial scheme but underestimate the ongoing scheme pressure from distributors and retailers.

- Salesmen subsidies: In many markets, the brand is expected to partially fund the distributor's salesman — either through a direct salary contribution or a “per-beat” allowance. This can add ₹5,000–₹15,000/month per salesman, depending on the market.

- Freight differentials: Shipping product to a distant state costs more per unit than local distribution. If you're manufacturing in Gujarat and distributing in Assam, freight can add 3–6% to your landed cost.

When you add these up, the total cost of distribution for a new brand in a new state is often 25–35% of MRP — not the 15–20% that most founders have in their pitch decks. For a full breakdown, see The True Cost of GT Distribution in a New State.

Sell directly to 40L+ kiranas — no GT network needed. Launch on Kirana Club's D2R Marketplace.

Explore the Marketplace →How to Build Your Pricing Architecture for a New State

If you're entering a new state, here is a practical 6-step process for building your pricing:

- Start from the retailer backward. What margin does the retailer need to stock and push your product? Research this by talking to 20–30 retailers in the target market. Don't assume — ask.

- Set the PTR based on competitive benchmarks. What does a comparable product in your category sell at to the retailer? Your PTR should be competitive — not necessarily cheaper, but within the range the retailer expects for your category and pack size.

- Calculate the PTS to give distributors a workable margin. Distributor margin expectations typically range from 6–12%, depending on the category and the volume you can guarantee. If your expected secondary is low, you'll need to offer higher margins to make it worth their while.

- Build in a scheme budget. Allocate 5–10% of your net sales for introductory trade schemes. This is not optional in a new market. Without schemes, retailers have no incentive to give you a first order.

- Stress-test your net realization. After PTR, PTS, schemes, freight, and expected returns — what is your actual margin per unit? If it's negative or razor-thin, you need to rethink your MRP, your pack size, or your market entry strategy.

- Plan for margin compression over time. As your brand gains pull, you'll have leverage to reduce retailer and distributor margins slightly. But in the first 12–18 months, expect to operate at higher distribution costs than your home market.

Schemes: A Tool That Becomes a Crutch

Trade schemes are necessary to enter a new market. But they become dangerous when they replace product-market fit. Watch for these warning signs:

- Sales spike during schemes but collapse after: This means retailers are buying on scheme, not because consumers are buying your product. You're funding inventory loading, not real demand.

- Distributors demand higher schemes every quarter: If the distributor's default request in every review meeting is “increase the scheme,” it means secondary sales are not self-sustaining. The product isn't pulling through.

- Competitors match your schemes within weeks: In commodity categories, scheme wars destroy margins for everyone. If your only differentiation is a bigger scheme, you're in a race to the bottom.

The goal of every scheme should be to drive first-time trial — not to sustain ongoing sales. If the product doesn't rotate on its own after the introductory scheme period, the problem is the product or the positioning, not the scheme budget.

For the full picture of how distribution economics work across the GT channel, read our Complete Guide to FMCG Distribution in India.