India has roughly 12 million kirana stores. No modern trade chain, no e-commerce platform, and no direct sales force can replace the density of that network. For a regional FMCG brand doing ₹50–₹500 Cr in revenue, general trade (GT) is not a channel — it is the business.

Yet most regional brand owners who have cracked their home market hit the same wall when they try to expand: the machine that worked in Rajasthan, or Maharashtra, or Tamil Nadu doesn't transplant to a new state cleanly. Distributors underdeliver. Retailers don't reorder. Working capital bloats. The brand retreats.

This guide is a complete map of how GT actually works in India — the economics, the execution, the failure modes, and what a modern expansion looks like.

What “FMCG Distribution” Actually Means

Distribution is not just “moving goods.” In GT, distribution means:

- Availability: Your product is physically present at the outlet when the consumer asks for it.

- Visibility: The retailer has placed it where it can be seen (not buried in a shelf).

- Rotation: It moves frequently enough that it doesn't die as dead stock.

- Replenishment: When it runs out, a new order comes fast enough that there's no gap.

- Economics: Every layer — distributor, retailer — makes enough to care about your product.

All five must work together. Brands that focus only on getting listed and ignore rotation and replenishment fail in 60–90 days.

The GT Channel Structure

India's general trade runs through a multi-layer system:

Brand → Super Stockist (optional) → Distributor → Retailer (Kirana) → Consumer

Each layer exists because it does a job:

| Layer | Primary Job |

|---|---|

| Super Stockist | State-level inventory buffer; bulk dispatch |

| Distributor | Retail coverage, credit to retailers, local schemes |

| Retailer | Consumer access; last-mile recommendation |

The sales team (TSI/salesman) sits between the distributor and retailer — visiting beats, taking orders, pushing schemes. This is the invisible layer that most brands underestimate when they expand. You're not just appointing a distributor. You're buying into a system that includes humans, credit, logistics, and trust.

GT vs Modern Trade vs E-commerce

| Channel | Reach | Margin Ask | Speed to Scale | Brand Control |

|---|---|---|---|---|

| GT (Kirana) | Highest (12M outlets) | Moderate–High | Slow to build | Low–Medium |

| Modern Trade | Urban/mid-tier cities | High (listing + promo) | Medium | High |

| E-commerce | Urban, young demographics | Variable | Fast to list, slow to scale | High |

| D2R Platform | GT retailers, tech-enabled | Leaner than traditional GT | Fast | High |

For brands targeting mass consumption categories — food, snacks, packaged staples, personal care — GT is still non-negotiable. MT and e-commerce are supplements, not substitutes.

Sell directly to 40L+ kiranas — no GT network needed. Launch on Kirana Club's D2R Marketplace.

Explore the Marketplace →Category Matters More Than Most Brands Admit

Not every FMCG category behaves the same in GT. This shapes everything from margin expectations to distributor type to retailer incentive.

High-frequency, low-ticket categories (namkeens, biscuits, small-pack beverages): Retailer cares most about rotation speed and impulse visibility. Margins of 15–20% are typical for new/regional brands. Distributor performance is measured by outlet coverage, not just volume.

Personal care and home care: Consumer trust and product familiarity matter more. Retailer needs to believe the consumer will ask for it. First-buy incentives and sampling are important. Distributor relationships with chemists or cosmetic retailers may be more valuable than a grocery distributor.

Dairy and perishables: Entirely different logistical animal — cold chain, shorter shelf life, daily replenishment. Distribution setup and economics are not comparable to shelf-stable FMCG.

Staples (atta, dal, oil, rice): Often category-specialist distributors. Price sensitivity is extreme. Retailer margins are tighter but volume is high. Brand pull needs years to build.

Know which game you're playing before designing your expansion.

The Margin Reality

The margin stack in GT is not fixed. It depends on:

- Your brand's pull strength (does the consumer ask for you by name?)

- Category velocity (how fast does this product rotate at the outlet?)

- New market vs. established market (new state = higher risk for retailer = higher margin demand)

A rough guide:

| Brand Type | Retailer Margin Expectation |

|---|---|

| National brand with strong pull | 5–10% |

| Regional brand with moderate pull | 10–18% |

| New brand entering unknown market | 18–25%+ |

Beyond retailer margin, the distributor's all-in cost (margin + credit losses + scheme funding + returns) often brings the total cost of distribution to 20–30% of the sale price for smaller brands. Most founders only count the number on the term sheet, not the total.

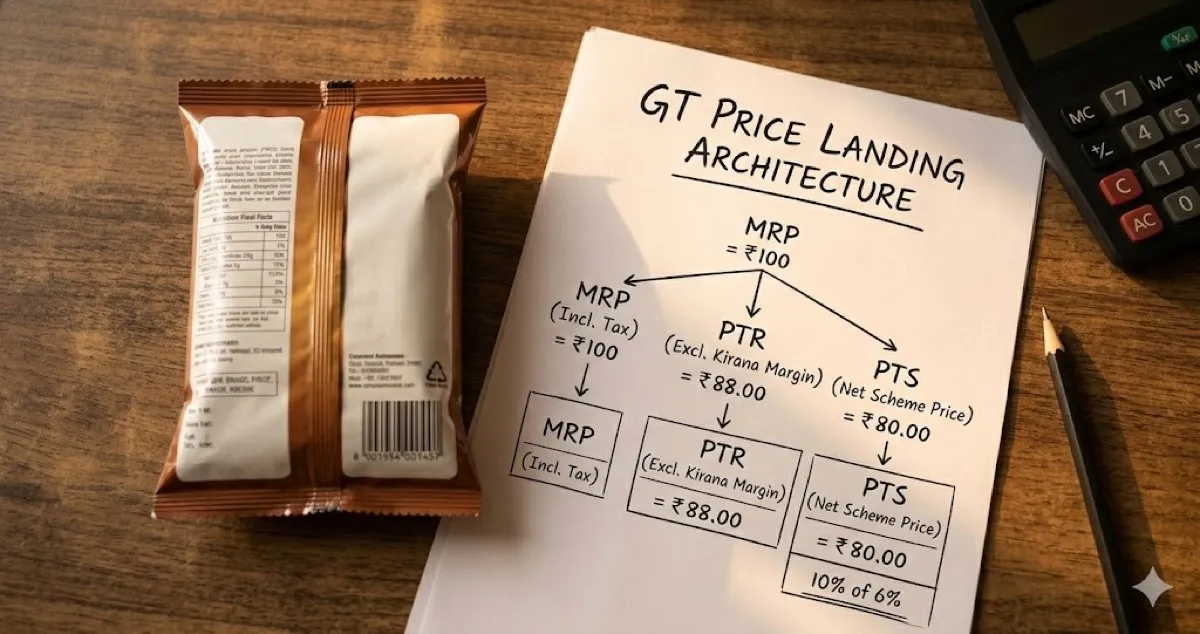

For a deeper breakdown, read What Margins Do Distributors and Kiranas Expect and GT Pricing Architecture: MRP, PTR, PTS Explained.

Working Capital: The Hidden Expansion Killer

Traditional GT expansion locks up working capital in two places:

- Distributor credit: Your goods move to the distributor, but cash comes back 15–30 days later (often 45+ days in new states with weak secondary).

- Schemes and damages: You fund schemes upfront; recovery is disputed and delayed.

If you're doing ₹1 Cr/month of sales in a new state with 30-day distributor credit and 15% scheme investment, you're carrying ₹30–40 Lakhs of locked capital per state — before you add team costs.

Scale that to 5 states and the working capital problem is a significant drain on your balance sheet.

Read more: Credit Risk and Collections in GT and The True Cost of GT Distribution in a New State.

Sell directly to 40L+ kiranas — no GT network needed. Launch on Kirana Club's D2R Marketplace.

Explore the Marketplace →The Shift Happening Right Now

India's GT channel is going through three simultaneous changes:

- Digital ordering: A meaningful portion of kirana orders are now placed via WhatsApp or apps. The beat-and-book model is not dead, but it's being augmented.

- Community-driven discovery: Kirana owners increasingly discover brands through retailer communities and peer recommendations, not just distributor push.

- Direct-to-Retailer (D2R) platforms: Brands can now reach retailers directly — without building a state-level distribution infrastructure first.

These changes don't make the traditional model irrelevant. They make it possible to test and enter markets faster and with less capital commitment before committing to a full distribution build.

Learn more: Direct-to-Retailer (D2R) in India's General Trade.

Where to Go From Here

This guide is the map. The articles below are the deep dives:

- Unit economics and pricing: GT Pricing Architecture Explained and What Margins Do Distributors and Kiranas Expect

- Market entry: How to Test a New Market and From Regional to PAN India: A Playbook

- Distributor management: How to Find and Appoint Distributors, Distributor Terms Sheet and Red Flags, Credit Risk and Collections in GT

- Retailer mechanics: How Kirana Stores Decide What to Stock, GT Demand Creation Without Burning Money

- Operations: Logistics and SLA in GT, How to Handle Returns, Expiry and Damages

- Decision frameworks: Super Stockist vs Distributor vs D2R, Why Regional Brands Fail When Expanding Nationally

- Checklists: 20 Questions Before You Enter a New State