A kirana owner has limited shelf space, limited cash, and no desire for experiments that don't move. Understanding how they think is the most underrated skill in GT expansion.

The Kirana Owner's Mental Model

A kirana store is not a passive distribution point. The owner is an active portfolio manager making daily decisions about:

- Which products to stock

- How much cash to lock in inventory

- Which brands to recommend when a consumer asks for “something similar”

- Which slow-moving products to return or stop reordering

Every decision runs through a simple filter: “Will this sell fast enough to get my money back, and then some?”

Everything else — loyalty to a distributor, interest in your brand story, appreciation for your packaging — is secondary to this question.

What Kiranas Optimize For (In Priority Order)

1. Rotation speed. If a product sits on the shelf for more than 4–6 weeks, it's “slow.” A new brand needs to earn a faster rotation cadence than this or it will be deprioritized.

2. Margin relative to rotation. A product that gives 20% margin but rotates once a month is worse than a product that gives 12% margin but rotates twice a week. Kirana owners understand return on inventory investment intuitively, even if they don't use that language.

3. Consumer recognition. Products the consumer asks for by name get stocked almost automatically. Products the retailer has to introduce require a higher margin to compensate for the selling effort.

4. Reliability of supply. A product that's out of stock or delivered unreliably gets replaced on the shelf. Shelf real estate is finite. If you can't keep it filled, a competitor will.

5. Credit support. In many GT markets, distributors offer 7–15 day credit to retailers. A brand that insists on cash upfront at the retail level (e.g., in a D2R model with prepayment) needs to compensate with higher margins or significantly better product pull.

6. Handling risk. Easy-to-damage, leaky, or fragile products create headaches. Kirana owners don't like products where they need to inspect every carton.

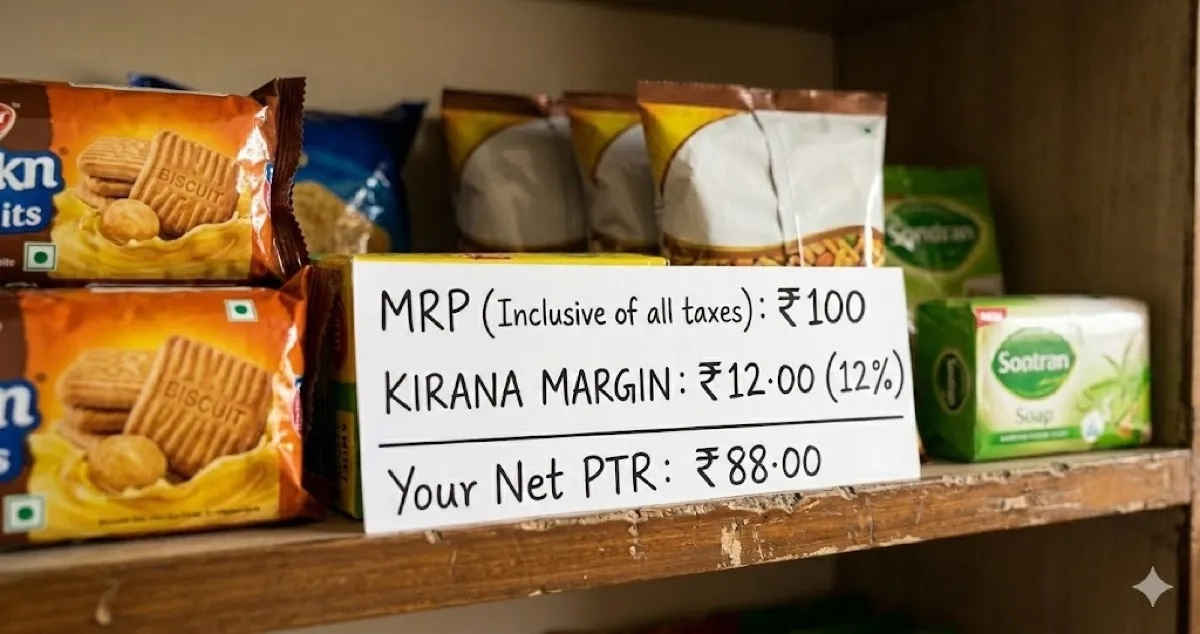

For a deeper look at how margins work across the GT chain, read our guide on FMCG distributor and kirana margins.

How New Brands Get on the Shelf: The Two-Stage Problem

Stage 1: Getting the first order

A retailer's first order from a new brand is essentially a risk transaction. They're trading cash or credit for uncertainty. What reduces that risk?

- A distributor relationship the retailer already trusts (salesman vouches for the new brand)

- An attractive trial margin that compensates for the uncertainty

- A small first order that doesn't require a large cash commitment

- A simple, clear product offering (not 30 SKUs on the first pitch)

- A free sample or trial unit that the retailer can evaluate before ordering

Stage 2: Getting the reorder

This is where most new brands fail. They get the first order. The retailer tries it. But the reorder doesn't come because:

- The product sold but the supply chain didn't replenish fast enough (retailer ran out before the next order cycle)

- The product didn't sell as expected (consumer didn't recognize it or competitor brand was right next to it)

- The distributor didn't follow up at the right time

The reorder is won by the product and the supply chain, not by the salesman's pitch.

Sell directly to 40L+ kiranas — no GT network needed. Launch on Kirana Club's D2R Marketplace.

Explore the Marketplace →Category-Specific Notes on Kirana Decision-Making

Snacks and packaged food: Impulse placement matters enormously. A product at the counter level gets seen 50 times a day. A product on a mid-shelf behind the counter gets seen 5 times. If you can't win counter-top placement (often paid via free units or scheme), your visibility in this category is severely handicapped.

Beverages: Chiller placement is everything in summer markets. If you're a regional beverage brand, ensuring your product is in the cooler (not just on a shelf) may require a chiller subsidy or co-investment — which changes your expansion economics significantly.

Personal care: Consumer brand preference is high and switching is slow. Getting into a new state means displacing something already on the shelf. Retailer margin needs to be strong because it's the retailer, not the consumer, who will introduce your brand.

Staples: Price and pack size are the primary decision criteria. Retailers will stock multiple competing brands to offer options. Getting listed is easier; getting rotation share is harder. Consistent quality matters more here than in impulse categories.

Three Practical Ways to Win a New Kirana

The “start small, prove first” approach: Lead with your top 2–3 SKUs, not your full range. Get those products rotating reliably. Then expand the assortment. Retailers who have experienced one positive cycle with you are 3–4x more open to adding more SKUs than first-time buyers.

The “community pull” approach: If 10 kiranas in a pin code are already successfully selling your product, the 11th kirana is much easier to convert. Retailer communities — especially digital ones — amplify this. A retailer who sees his peers talking about a product with good sell-through will want in.

The “earn the counter” approach: In impulse categories, invest in one thing first: counter placement. This requires an incentive (usually free goods or a scheme), but the visibility impact on first-time consumer trial is dramatically higher than shelf placement. Once consumers start asking for your product, the retailer's logic flips — now they need to stock you, not the other way around.

For the complete framework on FMCG distribution in India, read our comprehensive distribution guide. For strategies on creating demand at the retail level, see FMCG demand creation in general trade.