The distributor term sheet is not a formality. It's a conflict prevention document. Every clause you leave vague will become a dispute in 6 months.

Section 1: Territory Definition

What to define: Specific pin codes, districts, or cities. Not “West Maharashtra” or “Pune region.”

Why it matters: Ambiguous territories create channel conflict when two distributors claim the same outlet. Channel conflict destroys both distributors' incentive and creates retailer confusion.

What to avoid: Blanket state exclusivity given before performance is proven. Many brands give UP exclusivity to one distributor and then discover they can only reach 3 districts of 18. The state is locked, coverage is non-existent, and the distributor can legally claim you can't appoint anyone else.

Best practice: Start with city/district-level appointments. Add geography as coverage is proven.

Section 2: Exclusivity Terms

What to define: Exclusivity, if given, must be performance-linked. “Exclusive for Pune city, subject to achievement of 600 active outlets and ₹20 Lakhs/month secondary by month 6.”

Why it matters: Exclusivity without performance benchmarks is a free pass for underperformance. The distributor has no incentive to cover aggressively if your brand is captive.

What to avoid: “Exclusive for the state.” Full stop. This is the most common and most costly mistake in new state appointments.

Section 3: Pricing and Margins

What to define clearly:

- PTS (price to stockist): Your price to the distributor

- PTR (price to retailer): What distributor must sell at to retailer

- Retailer margin: Implied by PTR vs MRP

- Schemes: When, how, funded by whom, execution proof required

Common dispute: You run a “15% off” scheme for Q1. Distributor passes on only 10% to retailers and pockets the rest. Unless your term sheet specifies that scheme execution proof (secondary data + retailer receipts) is required for claim reimbursement, this happens regularly.

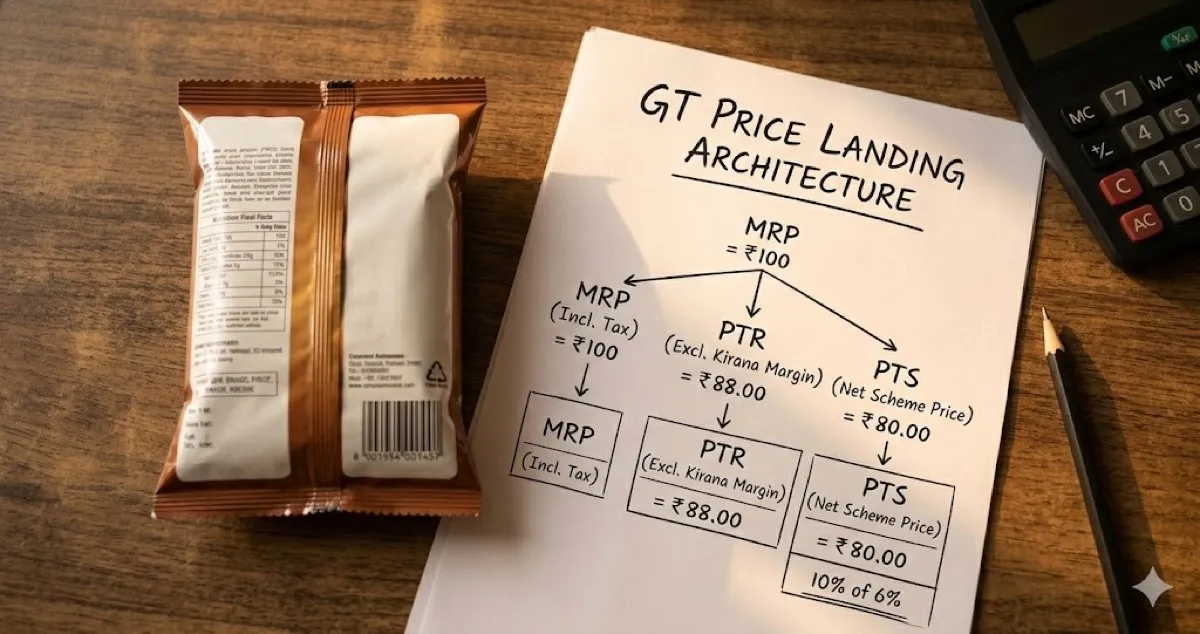

For a complete walkthrough of pricing structures, see our guide on GT pricing architecture: MRP, PTR, PTS, and schemes.

Sell directly to 40L+ kiranas — no GT network needed. Launch on Kirana Club's D2R Marketplace.

Explore the Marketplace →Section 4: Credit and Payment Terms

What to define:

- Credit period: Number of days from invoice date or delivery date (define which)

- Credit limit: Maximum outstanding at any time (prevents over-ordering)

- Late payment consequences: Supply hold after X days overdue

- PDC requirements: Some brands require post-dated cheques; define this upfront

Typical credit period: 15–30 days for established distributors in established states. In a new state, consider shorter initial credit until payment behavior is proven.

Critical clause: “Credit period begins from invoice date, not delivery date.” This single clarification prevents a common dispute where distributors claim the 30 days starts from when they receive goods (3–5 days after invoice), effectively extending credit by 5 days on every transaction.

For a deeper dive into credit risk management, read our guide on GT credit risk and collections.

Section 5: Returns, Expiry, and Damage Policy

Define:

- Return window: Maximum days post-purchase for any claim

- Expiry policy: Who bears the cost of near-expiry returns? (Common: brand bears cost within stated shelf life + 30 days; distributor bears cost if product was held too long)

- Damage claims: Photo/video documentation required within 24 hours of delivery. Claims without documentation will not be processed.

- Replacement vs. credit note: Which will you issue? Timelines?

The number to watch: A clean, well-run distributor relationship should have returns/damage claims below 2–3% of primary. If claims consistently run 8–10%+, either your packaging is failing or the distributor is making fraudulent claims.

For a complete guide to handling returns operationally, see how FMCG brands handle returns, expiry, and damages in GT.

Section 6: Secondary Data Sharing

What to define: Weekly secondary sales data (outlet-wise, SKU-wise) shared by a defined day of the following week.

Why this is non-negotiable: You cannot manage what you cannot see. A distributor who refuses to share secondary data has something to hide — either coverage is lower than claimed or sell-through is weak.

How to enforce it: Tie scheme reimbursement to secondary data submission. “Schemes for Month X will be reimbursed only upon submission of verified secondary data for Month X.” This is the most effective enforcement mechanism in practice.

Sell directly to 40L+ kiranas — no GT network needed. Launch on Kirana Club's D2R Marketplace.

Explore the Marketplace →Red Flags During Negotiation

| Behavior | What It Signals |

|---|---|

| Demands state exclusivity before first order | Opportunistic, not performance-oriented |

| Cannot or refuses to share retailer list | Coverage claims are overstated |

| Asks for high credit limit on day one | Likely to over-order for scheme benefit, then pay slowly |

| Brings up “other brands” as leverage constantly | Will do the same to you; loyalty is purely margin-driven |

| Vague on salesman count and beat frequency | Has limited infrastructure; will underdeliver |

| Avoids formalizing anything in writing | Prefers verbal flexibility to commit to nothing |

For a complete framework on FMCG distribution in India, read our comprehensive distribution guide. For guidance on finding the right distributors in the first place, see how to find distributors in India.